Comparing business banking and payments platforms that lower the cost and complexity of cross-border account management is harder than it should be. Most business payment platforms restrict multi-currency tools to premium plans, hide key pricing, or require complex onboarding for non-local companies. This comparison covers costs, account features, international coverage, and support models so businesses can pick a payment provider that fits their operational needs.

Table of Contents

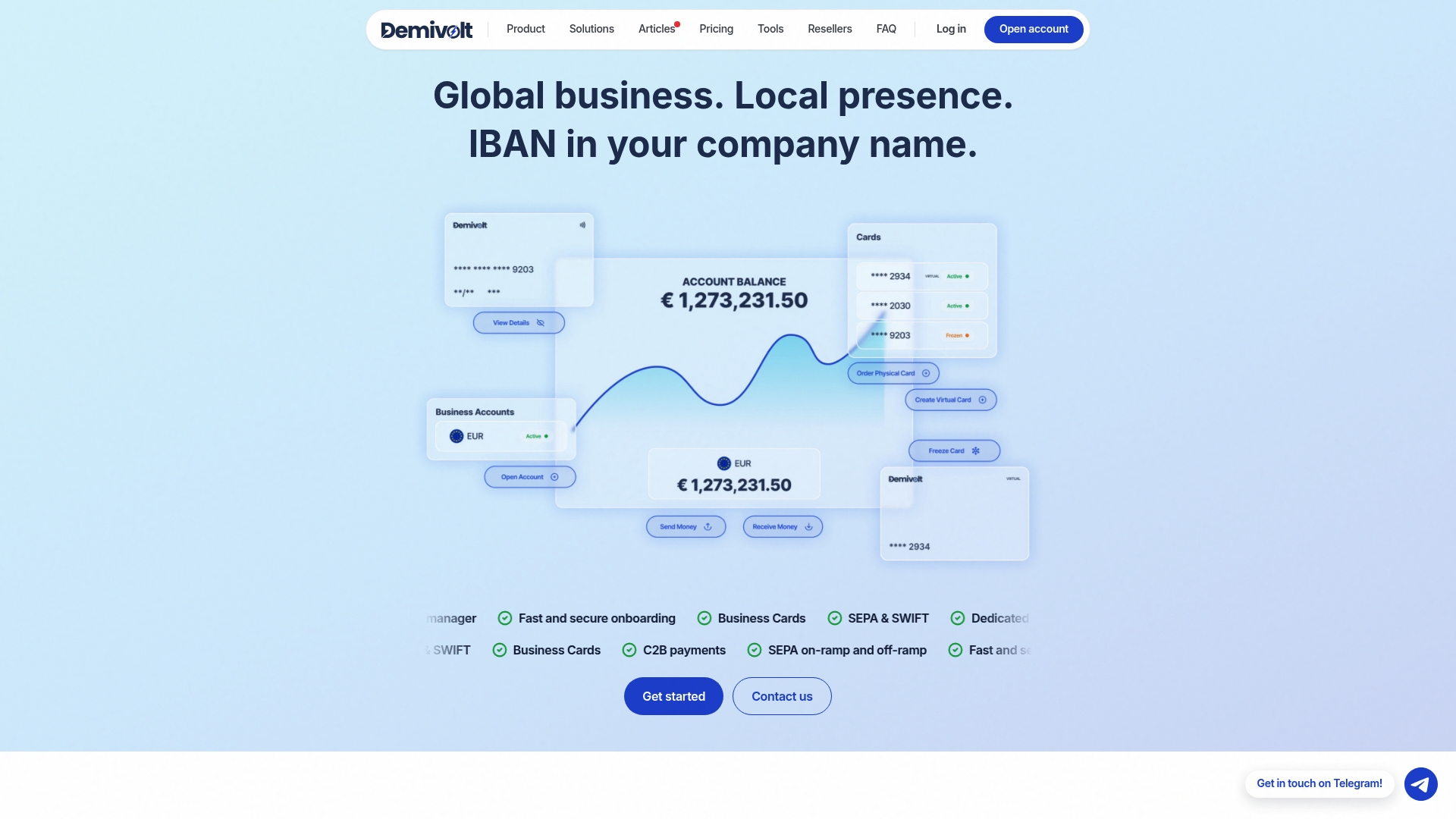

Demivolt

At a Glance

The vendor advertises outgoing SEPA transfers for €0.40 each. Demivolt pairs dedicated IBANs with SEPA and SWIFT rails for euro and cross-border flows. The platform targets companies that need compliant account structures and lower per-transfer costs for routine payouts.

Core Features

Demivolt issues dedicated IBANs and supports SEPA and SWIFT transfers, letting teams move euros and other currencies across borders. The product includes user role and permission management and SEPA on-ramp and off-ramp capabilities for external fund movement. Physical and virtual business cards are listed as coming soon, with current workflows focused on transfers and account management.

Key Differentiator

According to the company, Demivolt offers fully regulated EU-compliant business accounts with transparent fees and integration-ready infrastructure for cross-border payments. That positioning combines a focus on regulatory controls with payment rails and multi-account support suited to international operations.

Pros

That regulatory posture supports segregated client funds, which helps businesses meet compliance expectations while keeping treasury flows auditable. Transparent lower-cost transfer pricing reduces routine payment expense for EU operations. Fast onboarding and multi-account structures let teams create separate IBANs per business unit or client. The vendor also provides a reseller program to let advisors earn referral commissions.

Cons

- Cards are noted as “coming soon,” so current users rely primarily on bank transfer options.

Who It’s For

Demivolt fits regulated-aware small-to-medium businesses and international companies handling regular euro payments. If you run an EU digital service, e-commerce operation, or SME that needs segregated IBANs and multi-user access, this service matches those operational needs. High-risk business models should expect extra compliance steps.

Unique Value Proposition

Free account opening and low per-transfer fees lower the marginal cost of cross-border payouts. That cost profile helps teams that move volume in euros reduce banking overhead and reallocate budget to operations. For advisors, the reseller program creates a recurring referral revenue channel tied to client payment volumes.

Real World Use Case

A Lithuanian e-commerce company uses Demivolt to manage EU and international payments and to handle client refunds with fewer banking intermediaries. The team issues virtual cards for online advertising once card features arrive. Quick verification and separate IBANs simplify reconciliation across marketplaces and agencies.

Pricing

The vendor advertises free account opening and verification. Outgoing SEPA transfers are €0.40 per transfer. SWIFT transfers show €25 inbound and €30 outbound in the fee schedule. Fees apply to low-risk Lithuania-based clients; pricing varies by jurisdiction and risk profile.

Website: https://demivolt.com

FINCI Business Accounts

At a Glance

FINCI’s marketing materials state its cross border payments can be 8x cheaper than traditional banks. The company also advertises multi currency business accounts that include GBP, PLN, USD, and EUR. Onboarding is online and the vendor assigns dedicated account managers for tailored setups. That mix positions FINCI toward complex, international payment needs rather than simple domestic banking.

Core Features

FINCI provides multi currency accounts and connectivity to major payment rails including SWIFT and SEPA, enabling international transfers from a single interface. The platform includes user profile management with permission controls and mobile plus desktop access for payments, transfers, and account oversight. A range of Mastercard powered debit cards covers physical, digital, and co branded options for expense handling and crypto transactions.

Key Differentiator

FINCI focuses on businesses with complex cross border flows and multiple currency needs. The vendor emphasizes tailored account setups and personalized support, which aims to reduce friction for unusual business models. That combination of multi currency connectivity and account manager assistance separates it from simpler business accounts that only serve one region.

Pros

FINCI combines global transfer rails with account controls and card management, which simplifies running payments across several currencies. The platform claims cost advantages on cross border payments, a point that will matter to teams moving frequent international transfers. Personal account managers and a quick online onboarding process reduce setup time for companies with bespoke compliance needs.

Cons

- Limited pricing transparency: the vendor shares only a headline range and not detailed tiered fees or per transaction schedules.

- Security and data privacy details are not fully listed and third party reviewers advise verifying safeguards.

- Smaller or purely domestic businesses may find the feature set and permission controls more complex than necessary.

When It May Not Fit

If your company prefers face to face banking rather than an online onboarding flow, FINCI could feel awkward. Firms with simple single currency needs will not need the multi currency tooling and permission layers. Also expect fee variation by currency and volume, which may complicate budgeting for low margin operations.

Who It’s For

FINCI suits medium to large businesses engaged in cross border trade that need multi currency accounts and international payment rails. Financial managers who require role based access controls and card issuance will find the product relevant. The service also fits fintech companies that need tailored account setups and dedicated support.

Real World Use Case

A European startup with partners in North America and Poland uses FINCI to hold EUR and PLN, send SWIFT transfers, and pay contractors with company debit cards. The dedicated account manager configured permission roles for finance and operations staff. That setup reduced manual FX juggling and centralized card controls for the finance team.

Pricing

Plans run from €20 to €120 per month depending on the selected plan. The vendor notes additional fees may apply for certain transactions and card services. Detailed tier and transaction fee schedules are not publicly listed.

Website: https://finci.com

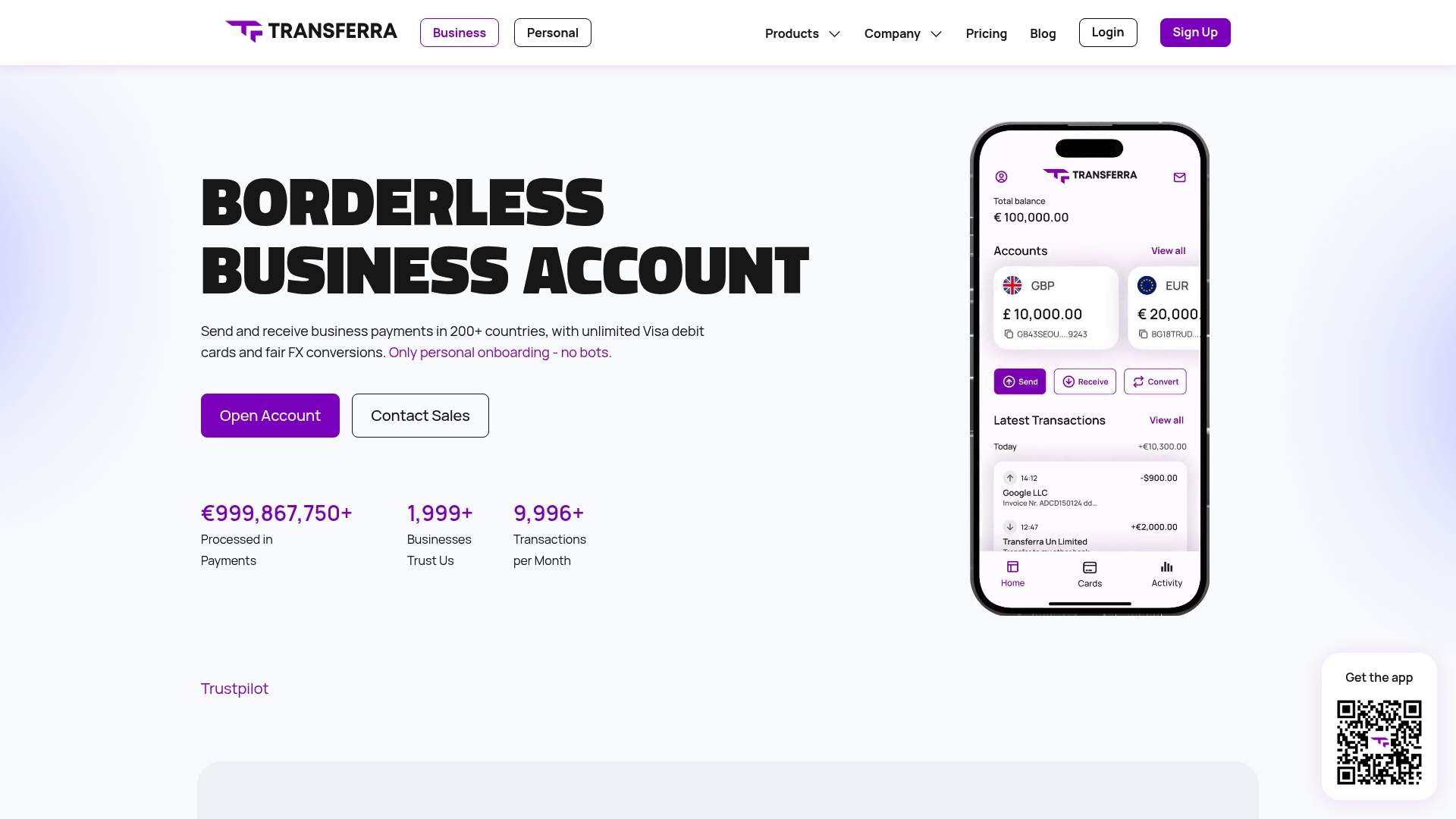

Transferra

At a Glance

Transferra reports business accounts that reach more than 200 countries. That global reach pairs with instant issuance of corporate Visa debit cards and local IBANs. The vendor emphasizes low foreign exchange fees and fast transfers across SWIFT, SEPA, and local rails.

Core Features

Transferra combines borderless business accounts with instant issuance of unlimited corporate Visa debit cards and virtual card options. It provides local IBANs for faster domestic payments, multi currency handling, and currency exchange at lower rates. The platform also offers API integration and support for complex corporate structures and non UK resident companies.

Key Differentiator

Transferra stands out for fully digital onboarding and the ability to provide local IBANs in multiple jurisdictions during setup. That instant setup reduces wait time for account activation and local payment routing. The package pairs low FX pricing with dedicated account managers on higher tiers for hands on support.

Pros

Support for many currencies and cross border payments reduces routing friction for international suppliers and payroll. The vendor advertises low FX fees and transparent pricing, which helps you predict conversion costs. Premium plans include dedicated account managers who handle compliance and complex corporate needs. The online onboarding process is fast and keeps documentation work to a minimum.

Cons

-

Pricing can vary with company complexity and volume, which may raise costs for very small or early stage businesses.

-

API access and bulk payment capabilities are limited or gated behind higher tiers, so developers may need to budget for upgraded plans.

-

Public detail on consumer complaints or specific operational limits is sparse, making independent risk assessment harder.

When It May Not Fit

If you run a very low volume startup with tight monthly bills, Transferra’s plan structure may cost more than a basic local business account. If you need full API and bulk payment features on a low tier, this product will feel restrictive. Detailed operational limits and complaint histories are not specified, so some treasury teams may prefer a provider with more public transparency.

Who It’s For

Transferra fits international small to large businesses that need multi currency accounts and local payment routing. It also suits non UK resident companies and firms with layered corporate structures that require a dedicated compliance contact. Teams that value quick digital onboarding and virtual card issuance will find it especially useful.

Real World Use Case

A digital marketing agency billing clients in euros and dollars uses Transferra to hold multiple currencies and issue virtual cards to contractors. The agency routes supplier payments through local IBANs to lower fees and shorten settlement time. Dedicated account support handled complex shareholder documentation during onboarding.

Pricing

Plans vary by business size and complexity, with pricing tiers for local and international use. Pricing starts from €49/month for local businesses and rises to €149/month for international plans. Transferra also offers custom quotes for complex corporate setups.

Website: https://transferra.uk

Qonto

At a Glance

Qonto reports a Trustpilot score of 4.8 out of 5 from over 57,000 reviews. The vendor also states accounts can open in 10 minutes. Those two claims explain why small businesses often choose a digital first business account for day to day finance work.

Core Features

Qonto combines local IBAN accounts, multi currency payments, and SEPA plus international transfers with Wise integration. It issues virtual and physical Mastercard cards and offers automated compliant invoicing, expense approvals, and real time cash flow and VAT tracking. The vendor states it connects with over 2,000 external tools for bookkeeping and automation.

Key Differentiator

The main differentiator is an end to end financial management stack that pairs fast onboarding, focused security measures, and high reported customer satisfaction. That satisfaction figure above and the quick account setup make it practical for founders who need usable finance controls from day one. Customer support and compliance features reinforce that positioning for small firms.

Pros

That score and that ten minute claim point to a positive customer experience. Support includes 24/7 human assistance in France and transparent billing with no hidden fees. Combined card controls, invoicing automation, and VAT tools reduce manual bookkeeping work for small finance teams.

Cons

- Potentially higher costs when you add advanced modules such as automated invoice collection and expense workflows.

- Some international transfers incur fees, especially for uncommon currencies.

- Acts as a regulated payment institution, not a full service bank, so treasury and lending products are limited.

When It May Not Fit

Not suitable for large enterprises that need full banking services, treasury desks, or bespoke lending solutions. Teams with heavy non standard currency flows may face higher fees for international transfers. Organizations that require branch banking or complex corporate finance products will likely find the offering too limited.

Who It’s For

Small business owners, startups, and SMEs that want a fast business account and online finance controls. Teams that need multi user access, card controls, and integrated invoicing will benefit most. Entrepreneurs who value quick onboarding and responsive support match this product profile.

Real World Use Case

A three person startup opens a Qonto account in minutes and issues virtual cards for contractors. They automate invoices, route payments through Wise for currency conversion, and monitor VAT and cash flow in real time. That setup reduces manual reconciliation and speeds month end reporting.

Pricing

Plans start at €9/month for basic accounts, with Smart at €19/month and Premium at €39/month. Monthly billing is available along with annual options, and add ons increase costs for advanced collections and automation.

Website: https://qonto.com

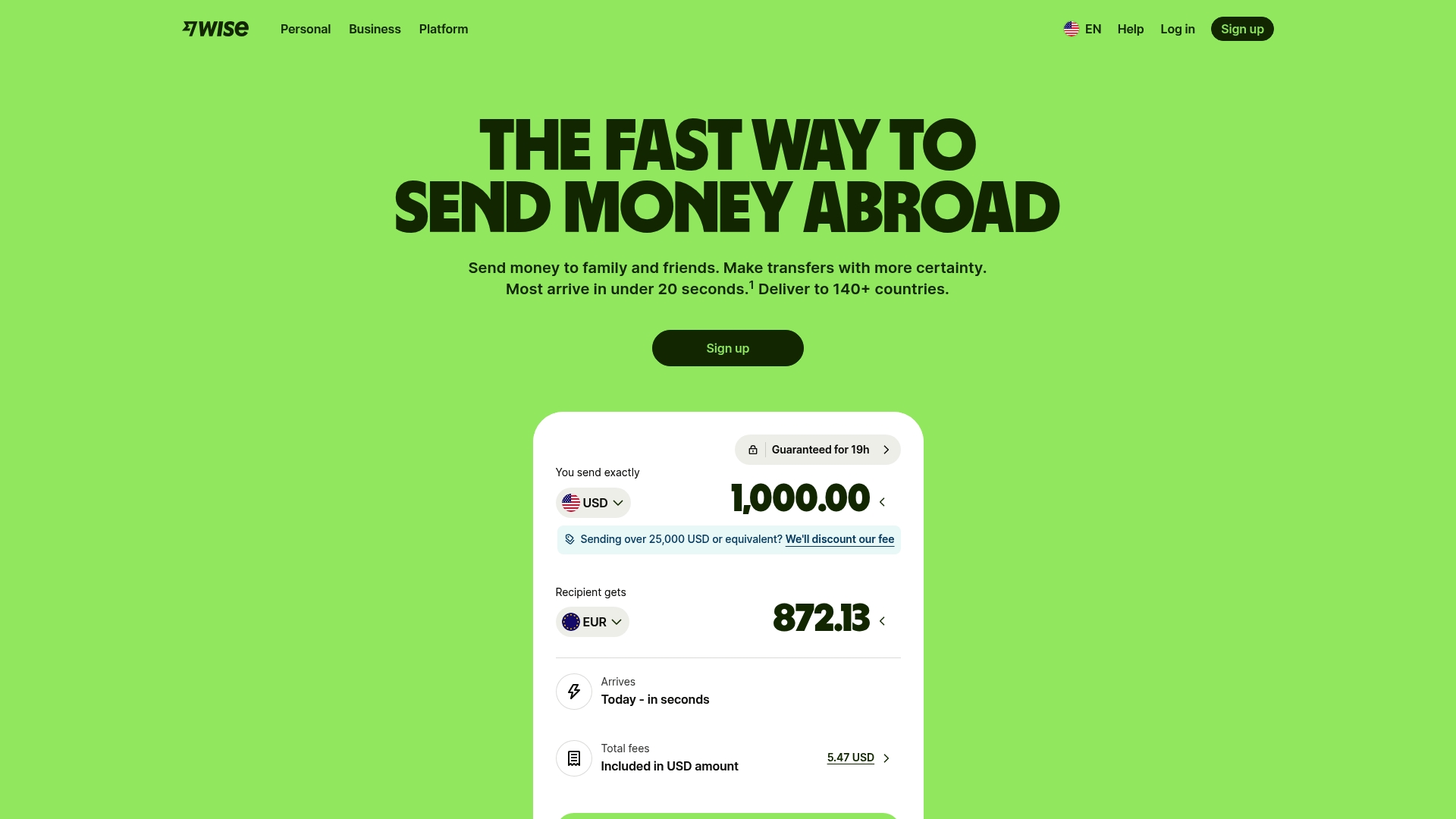

Wise

At a Glance

Wise’s marketing materials state most transfers arrive under 20 seconds, a claim that catches attention for cross border payments. According to the company, interest accounts offer up to 3.14% APY in select currencies. The vendor advertises optional FDIC passthrough insurance up to $250,000 for eligible US funds.

Core Features

Wise supports international money transfers using mid market exchange rates and an upfront fee schedule, which reduces hidden costs on large transfers. The account lets you hold and convert balances in multiple currencies and receive local account details in many major currencies. The service includes a debit card for global spend, integrations with accounting software, and customer support available 24/7.

Key Differentiator

Wise stands out for its claim of using real exchange rates with no hidden markup and for showing fees before you confirm a transfer. That transparent fee display changes how you compare bank costs and third party providers. For businesses that run frequent cross border payouts, that clarity reduces billing surprises.

Pros

Transparent pricing and the mid market rate approach make it easy to forecast FX costs for vendor payments. Competitive fees matter most on larger transfers, and the fee model rewards volume with lower relative cost. Robust compliance controls, segregated accounts, and fraud detection help keep funds secure while providing business features like multiple currency balances and pay in local currency.

Cons

- Interest earnings and certain account features are not available to all residents or in every state. This limits who can access savings features.

- Service availability varies by country and banking jurisdiction, which can block either sending or receiving in some corridors.

- During demand spikes, customer support can experience delays, which may slow resolution of time sensitive payment issues.

When It May Not Fit

If you require every banking feature in a single regulated bank wrapper, Wise may fall short because it is not a bank in most markets. Businesses that need guaranteed deposit insurance in all jurisdictions will face gaps because that FDIC coverage depends on location and account routing. Companies that need embedded cash management services unique to full service banks should look elsewhere.

Who It’s For

Businesses and individuals who move money across borders regularly and want predictable fees and fair exchange rates will find value. Small to medium sized exporters, remote teams, and service providers who invoice in multiple currencies will benefit from local receiving details and multi currency balances. Organizations that need full domestic bank services in every market will not find a complete replacement here.

Real World Use Case

A US based small business pays suppliers in euros and pounds and receives client invoices in GBP. Using Wise reduced the companys FX markup and simplified reconciling invoices because transfers arrived quickly and fees were shown upfront. The team used the multi currency balances to time conversions around favorable market moments.

Pricing

Wise uses a transparent fee structure where costs vary by transfer amount and payment method. The company states discounts apply above certain thresholds, which reduces unit cost for larger payments. No flat rate is listed publicly because fees depend on route and funding type.

Website: https://wise.com

Revolut Business

At a Glance

Revolut Business’s marketing materials state it supports 25+ currencies, which lets teams hold and move money without constant conversions. The vendor also advertises regulation as a bank in the UK and licensing in the EEA. That combination targets companies that run cross-border operations and want consolidated accounts for multiple currencies.

Core Features

Revolut Business combines global payments with currency exchange at interbank rates and multi-currency accounts that let you receive, hold, and send funds in many currencies. The platform adds spend management with approval controls and automation for expense workflows. It accepts online and in-person payments and issues cards for teams while integrating with major accounting tools.

Key Differentiator

Built for global business efficiency, Revolut Business pairs regulated banking services in certain jurisdictions with multi-currency account management and automation features. That focus helps companies reduce manual reconciliations when they operate in multiple markets.

Pros

The product bundles payments, currency exchange, and expense controls in one place, reducing the number of vendor relationships finance teams manage. Multi-currency handling and interbank-style exchange rates lower conversion friction for international receipts and payouts. The platform supports automation for approvals and expense reporting, which speeds month end. It also offers deposit protection via its UK banking regulation for eligible balances.

Cons

- Pricing and plan features vary by region and by plan level, which makes comparisons across countries tricky.

- Several advanced capabilities live behind premium paid plans, so smaller teams may need to upgrade to get certain automation or payment features.

- The regulatory model differs outside the UK and EEA, and some services are delivered through partner banks rather than directly.

When It May Not Fit

If your business requires a full traditional banking relationship in every jurisdiction you operate, this platform may not match that requirement. Companies that cannot afford higher-tier plans will lack some advanced automation and payment options. Firms strictly tied to local deposit insurance rules outside the UK and EEA should verify coverage before committing.

Notable Integrations

Revolut Business integrates with Xero, Sage, and QuickBooks, and the vendor reports connections to more than 45 additional tools. Those integrations cover accounting, invoicing, and some ecommerce platforms, helping keep ledger entries aligned with card spend and bank movements.

Who It’s For

Businesses of all sizes that need global banking and payments, particularly those sending and receiving funds in multiple currencies. Finance teams that want built-in expense controls and accounting integrations will see the most immediate benefit.

Real World Use Case

A UK-based startup uses Revolut Business to handle multi-currency sales, automate team expense approvals, and push transactions into its accounting package. That setup reduces manual reconciliation and speeds access to foreign receipts for payroll and supplier payments.

Pricing

Plans start from £10/month for basic business accounts, with higher tiers adding more transaction allowances and automation. Enterprise customers can negotiate custom solutions and pricing.

Website: https://revolut.com/business

Comparison of alternatives

Comparing options for business banking and payments reveals trade-offs between fee structures, compliance designs, and available tools. Demivolt.com emphasizes simplicity and regulation in euro SEPA transfers, while competitors highlight diverse strengths such as multi-currency flexibility and card issuance.

Fee Transparency and Compliance Support

Demivolt.com offers clear pricing for SEPA transfers at €0.40, simplifying cost prediction for euro flows. Its focus on compliance and management of segregated funds fits EU-regulated businesses managing multiple IBANs. Conversely, FINCI provides multi-currency accounts with tailored onboarding; this enhances support for diverse international payment needs but lacks immediate fee detail visibility. This distinction allows informed decisions on fit for regional versus global operations.

Multi-Currency and Card Capabilities

TRANSFER balances an extensive set of payment rails alongside rapid virtual card issuance, benefiting teams needing fast access to payment tools for international supplier operations. Revolut Business supports intricate interbank rate exchanges and spend tracking systems via integration packages. Teams prioritizing operational support might lean towards these dynamic environments, sacrificing discrete euro SEPA options.

Best fit

- European-regulated businesses needing dedicated IBANs and SEPA transfer clarity benefit from Demivolt.com’s regulated efficiency.

- Cross-border organizations requiring multi-currency balance flexibility and tailored onboarding fit FINCI Business solutions.

- Transfer-heavy international businesses needing virtual cards quickly prefer Transferra for operational ease.

- SaaS startups leveraging streamlined invoice automation engage better with Qonto’s tool integration environment.

- Global exporters requiring upfront fee schedules for time-sensitive payments benefit from Wise’s detailed forecasting and rapid execution.

Our pick

Demivolt.com excels at simplifying euro-focused payment management for EU-regulated entities. Dedicated IBAN issuance paired with competitively low SEPA fees supports cost reduction and transparency for compliant operations. While alternatives cover broader scopes and currency handling, Demivolt.com remains distinct for organizations whose critical operations focus on strictly regulated euro transfers.

The following table compares various business banking platforms based on their ability to support international transactions and manage multi-currency accounts effectively.

| Platform | Key Features | Pricing | Best For | Limitation |

|---|---|---|---|---|

| Demivolt | Dedicated IBANs, SEPA & SWIFT payments, reseller program | SEPA €0.40/transfer | Small-medium businesses in the EU managing euro payments | Cards feature is forthcoming |

| FINCI | Multi-currency accounts, dedicated account managers | €20–€120/month | Medium-large businesses with complex international flows | Limited pricing detail and privacy transparency |

| Transferra | Instant IBAN issuance, multi-currency handling | €49–€149/month | SMEs requiring local and international banking | Advanced features gated behind higher-tier plans |

| Qonto | Local IBANs, Wise integration, VAT tracking | €9–€39/month | Small startups needing quick setup and integrated accounting | Limited advanced corporate banking features |

| Wise | Transparent FX rates, multi-currency holding | Fee per transaction | Businesses conducting frequent cross-border payments | Limited feature availability based on jurisdiction |

| Revolut Business | Multi-currency accounts, expense management automation | £10/month+ | Global businesses with regulatory banking in the UK | Advanced features need higher-tier plans |

How Do You Manage Costs and Compliance When Searching for Narvi.com Alternatives?

Choosing the right payment platform for your international business means balancing compliance, cost transparency, and ease of use. Many companies seek solutions that provide dedicated IBANs, lower transfer fees, and digital-first infrastructure designed for multi-account management and clear regulatory adherence. Demivolt meets those needs with a regulated European fintech platform tailored for businesses handling cross-border payments and multi-currency flows.

Demivolt offers fast onboarding, transparent fees, and segregated accounts to safeguard your funds. It supports SEPA and SWIFT transfers alongside user permission controls and multi-account structures that fit SMEs, digital services, and international teams. Learn how Demivolt reduces payment expenses and strengthens financial control at Demivolt. Take the next step to open your compliant business account and manage transfers with confidence.

FAQ

What features make Demivolt a good choice for businesses looking for payment solutions?

Demivolt offers dedicated IBANs and supports SEPA and SWIFT transfers, allowing teams to manage euro and other currency transactions efficiently. Its structured pricing includes €0.40 for outgoing SEPA transfers, making it cost-effective for routine payouts. Businesses seeking compliant account structures will find Demivolt’s features ideal for their operational needs.

How does Demivolt compare to FINCI for handling multi-currency payments?

FINCI supports multi-currency accounts and emphasizes personalized account management for complex scenarios. Companies needing a tailored approach for diverse payment functions may find value in FINCI. However, for small-to-medium businesses focusing primarily on compliant euro transfers, Demivolt offers lower transfer fees and a focused service structure that meets routine operational needs.

Can I manage user roles and permissions with Demivolt?

Demivolt provides user role and permission management, enabling teams to customize access for various users effectively. This feature supports operational efficiency and compliance by ensuring appropriate access control for different business units, making it a practical choice for businesses requiring structured control.

Are there any limitations to Demivolt’s service that I should be aware of?

While Demivolt offers strong features for euro transactions, its primary services currently focus on SEPA and SWIFT transfers, with physical and virtual cards labeled as “coming soon.” Businesses that require immediate access to card features may need to consider this aspect when evaluating their options.

What is the typical cost associated with using Demivolt for transfers?

Demivolt charges €0.40 for each outgoing SEPA transfer and has a pricing structure that is designed to reduce routine payment expenses. This cost-effective model can benefit businesses that handle high transaction volumes, allowing them to manage their payment costs effectively.